You just landed your first job in Dubai or your H-1B came through and you moved to New Jersey or you have been in London for eight years and you still have a savings account in India from your resident days. At some point – usually when you try to send money home, receive rent from your Indian property or move savings back to your overseas account – someone says: “You need an NRE account or maybe an NRO. Have you considered FCNR?”

And suddenly you are reading about three different accounts, none of which existed in your financial life before you moved abroad, all of which have different rules, different tax treatments and different consequences for getting them wrong.

Most NRIs spend years using the wrong account for the wrong purpose – depositing Indian rental income into their NRE account (a FEMA violation), keeping all their foreign savings in an NRO account (unnecessary tax liability) or ignoring FCNR entirely (and watching rupee depreciation quietly erode their returns).

This guide explains everything – clearly, practically and with real examples – so you never make those mistakes.

Tax consequences: Interest on NRO accounts is taxed at 30% (plus cess) in India with TDS deducted at source. Interest on NRE and FCNR accounts is completely tax-free in India. Putting the wrong money in the wrong account can create unnecessary Indian tax liability.

Repatriation consequences: Money in an NRE or FCNR account can be moved abroad at any time, without limits, without CA certificates, without documentation beyond a basic bank request. Money in an NRO account can only be repatriated up to USD 1 million per financial year and requires Form 145 (previously Form 15CA) and Form 146 (previously Form 15CB – a CA certificate) and full tax compliance before the bank will process the transfer. One decision about which account to use affects how easily you can access your own money years later.

FEMA compliance consequences: Depositing Indian-sourced income into an NRE account or continuing to use a resident savings account after becoming an NRI – are violations of the Foreign Exchange Management Act, 1999. The consequences range from bank account freezes to formal compounding proceedings with the RBI.

One Rule that Governs All Three Accounts

Before explaining each account, here is the single most important principle to understand:

The source of money determines which account it belongs in.

- Money you earned abroad → NRE or FCNR

- Money you earned in India → NRO

This one rule, applied consistently, prevents 90% of NRI banking mistakes. Keep it in mind as you read everything below.

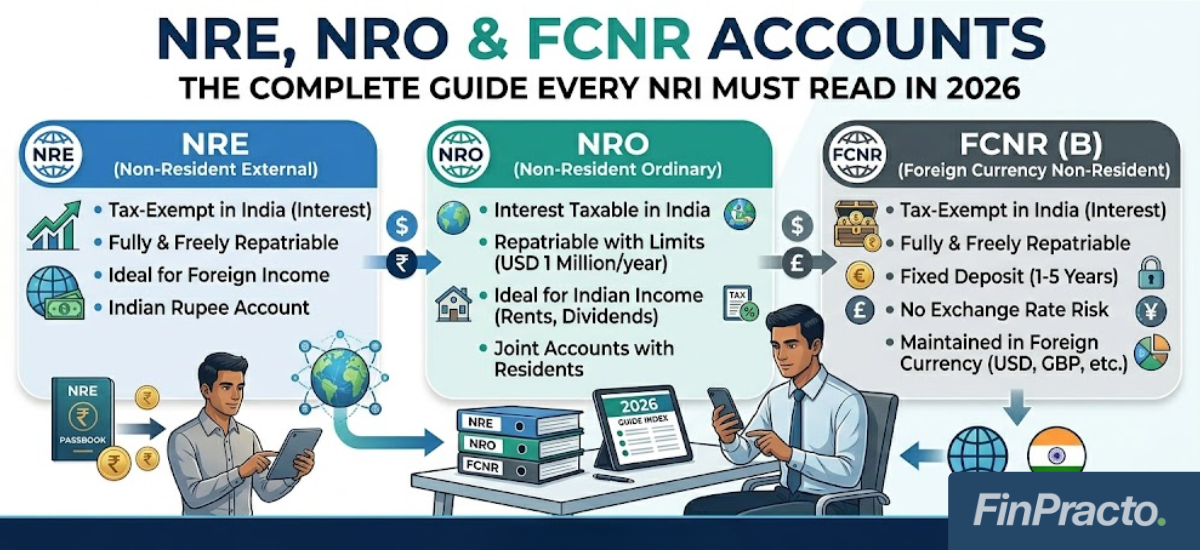

Part 1: The NRE Account – Your Foreign Earnings in India, Tax-Free

What Is It?

A Non-Resident External (NRE) account is a rupee-denominated bank account that holds money you earned outside India – your foreign salary, your overseas business income, proceeds from foreign investments – which you want to bring into India.

When you transfer money from your Dubai or New Jersey bank account to your Indian NRE account, the foreign currency is converted to Indian Rupees at the prevailing exchange rate and held in your NRE account.

The Three Things That Make NRE Special

Fully tax-free interest in India: Interest earned on NRE savings accounts and NRE fixed deposits is completely exempt from Indian income tax under Section 10(4) of the Income Tax Act. No TDS is deducted. No tax is owed. You keep every rupee of interest.

Fully repatriable – without limits or documentation: Both the principal you deposited and all interest earned can be transferred back to your overseas bank account at any time, with no upper limit, no CA certificate, no Form 145 or Form 146 needed. You submit a simple bank request and the money moves. This is the single most important operational advantage of the NRE account.

Joint holding allowed with other NRIs: You can hold an NRE account jointly with another NRI. You cannot, however, hold it jointly with a resident Indian – which is a common misconception.

- Inward remittances from abroad in foreign currency (your salary transferred from overseas)

- Transfers from another NRE or FCNR account

- Proceeds from foreign currency brought into India through banking channels

- Interest earned on the NRE account itself

What cannot be deposited:

- Indian rental income

- Indian salary (for services rendered in India)

- Indian dividends, interest from Indian FDs or proceeds from Indian asset sales

- Any income that arose in India

Depositing Indian-sourced income into an NRE account is a FEMA violation – even if the amounts are small and the intention was innocent. If your tenant pays rent into your NRE account directly, you are non-compliant.

Many returning NRIs continue to hold NRE accounts and claim the interest exemption after becoming full residents. This is incorrect and carries penalty exposure.

Part 2: The NRO Account – Your Indian Income, Managed Properly

What Is It?

A Non-Resident Ordinary (NRO) account is a rupee-denominated account designed to hold income that arises in India – rental income, dividends from Indian companies, pension, interest from Indian fixed deposits, proceeds from selling Indian assets.

Every NRI who has any source of income in India must have an NRO account. If you own a property in India that generates rent, that rent goes into your NRO account. If you receive dividends from Indian stocks, they go into your NRO account. If you inherited money from a family member in India, it goes into your NRO account.

The Critical First Step Most NRIs Delay

When you become an NRI, your existing resident savings account must be converted to an NRO account. It cannot simply remain open as a resident account. It cannot be converted into an NRE account either. Only conversion to NRO is permitted.

This conversion should happen as soon as you become an NRI. Many people delay it for months or years – which means they are technically non-compliant with FEMA for the entire period they continue using the resident account.

The process is simple: Inform your bank of your NRI status and request conversion to NRO. The account number typically stays the same. The account type changes but every month of delay is a period of non-compliance.

This is significantly higher than what a resident Indian pays – which is why the account structure decision matters.

To claim the DTAA rate instead of 30%, you must:

- Obtain a valid Tax Residency Certificate (TRC) from the tax authority of your country of residence

- File Form 41 (previously Form 10F) electronically on the Indian income tax portal

- Submit both documents to your bank before TDS is deducted

Many NRIs realise too late that 31.2% of their interest is being “eaten” by TDS and always check whether DTAA benefits can be applied. If you have not submitted your TRC and Form 41 (previously Form 10F), your bank is legally required to deduct at 30%. The excess can be reclaimed through ITR filing – but that is a refund process that takes months.

Repatriation From NRO – The USD 1 Million Rule

NRO account repatriation is limited to USD 1 million per financial year (April to March) after tax compliance and submission of required documentation.

This limit covers all your NRO accounts combined, across all banks. If you have NRO accounts at HDFC, SBI and ICICI, the USD 1 million limit applies to the total of all three.

To repatriate from your NRO account, you need:

- Form 145 (previously Form 15CA) – Filed online by you on the income tax e-filing portal before the transfer. This is a self-declaration of the remittance details and tax position

- Form 146 (previously Form 15CB) – A certificate issued by a Chartered Accountant confirming that all applicable taxes on the amount have been paid or provided for

- Proof of source of funds (sale deed, FD maturity certificate, rental agreement, etc.)

- Bank’s FEMA declaration / A2 form

- Passport and PAN copies

- Missing Form 145 before initiating an NRO repatriation causes transfers to get rejected at the bank level – sometimes repeatedly – before the missing step is identified.

The NRO to NRE Transfer Option:

You can transfer funds from your NRO account to your NRE account – which then gives you full repatriability without the USD 1 million cap. However, this NRO-to-NRE transfer itself counts against your USD 1 million annual limit and requires the same Form 145 / Form 146 (previously Form 15CA / Form 15CB) documentation. It is not a way around the limit – it is the limit.

When Does NRO Repatriation Exceed USD 1 Million?

If you need to repatriate more than USD 1 million in a financial year – for example, after selling a high-value property – you need RBI approval. This is obtained by submitting an application through your bank to the Reserve Bank of India, with full documentation of the source of funds and tax compliance. The process is procedurally intensive but not impossible.

Part 3: The FCNR Account – Protecting Your Foreign Savings From Rupee Risk

What Is It?

A Foreign Currency Non-Resident Bank account – commonly called FCNR or FCNR(B) – is a fixed deposit held in foreign currency in India. Unlike NRE and NRO accounts (which are rupee-denominated), FCNR deposits stay in the currency you deposited – USD, GBP, EUR, JPY, AUD, CAD and other freely convertible currencies accepted by your bank.

There is no currency conversion when you deposit and no currency conversion when you withdraw. The exchange rate risk is completely eliminated.

Why FCNR Matters: The Rupee Depreciation Problem

Every NRI who holds NRE fixed deposits faces a silent risk: Rupee Depreciation.

Say you deposit USD 10,000 in an NRE account today when the exchange rate is ₹83 per dollar. Your NRE FD earns 7% per year. In 2 years, your rupee balance has grown – but if the rupee has depreciated to ₹88 per dollar, your effective USD returns are significantly reduced and may even be negative in real terms.

FCNR deposits help preserve capital value when the rupee shows weakness by holding deposits in foreign currency itself. With FCNR, you deposit USD 10,000. You earn interest in USD. You withdraw in USD. You have no rupee exposure whatsoever.

FCNR – The Key Features

Tax-free interest in India: Interest earned on FCNR deposits is completely tax-free in India. No TDS is applied. Like NRE accounts, FCNR interest is exempt under Indian income tax law.

Fully repatriable without limits: FCNR accounts allow for full repatriation of both principal and interest without any limits. No USD 1 million cap. No CA certificate required. No Form 145 / Form 146 needed.

Fixed deposit only – not a savings account: FCNR is only available as a fixed deposit, not as a regular transaction account. You cannot use it for day-to-day payments or transfers.

Minimum tenure 1 year, maximum 5 years: FCNR deposits have a minimum tenure of 1 year and a maximum of 5 years. No interest is paid if the deposit is withdrawn within 1 year. If withdrawn after one year but before maturity, interest may be paid at a reduced rate or with a penalty.

Minimum deposit: Typically, around USD 1,000 or equivalent in other currencies (varies by bank).

Currencies accepted: USD, GBP, EUR, JPY, AUD, CAD and other freely convertible currencies as notified by RBI. Always confirm with your specific bank.

Who Should Use FCNR?

FCNR is most valuable for:

- NRIs who want to park foreign savings in India for a fixed period without taking rupee risk

- NRIs with USD, GBP or EUR earnings who want Indian bank security with foreign currency returns

- NRIs who anticipate needing to repatriate funds freely without the USD 1 million NRO limit

- NRIs in the RNOR period (after returning to India) who want to continue holding foreign currency deposits tax-free while RNOR status lasts

What Happens to Your FCNR When You Return to India?

When an NRI returns to India and becomes a resident, the FCNR deposit can be converted into a Resident Foreign Currency (RFC) account, allowing continued holding of foreign currency in accordance with FEMA rules. The RFC account can be maintained until the deposit matures, after which it follows resident account rules.

The Master Comparison Table

| Feature | NRE Account | NRO Account | FCNR Account |

| Currency | Indian Rupee | Indian Rupee | Foreign Currency |

| Who can open | NRI / PIO / OCI | NRI / PIO / OCI | NRI / PIO / OCI |

| Source of funds | Foreign income only | Indian income; also foreign | Foreign income only |

| Account type | Savings / Current / FD | Savings / Current / FD | Fixed Deposit only |

| Interest taxation | Tax-free in India | Taxable at 30% (TDS) | Tax-free in India |

| Repatriation | Fully free, no limits | USD 1M/year limit | Fully free, no limits |

| CA certificate needed to repatriate | No | Yes — Form 146 (previously Form 15CB) | No |

| Rupee depreciation risk | Yes | Yes | No |

The Five Most Common NRI Banking Mistakes and How to Avoid Them

However, Indian rental income must go into the NRO account. Depositing it into NRE is a FEMA violation that can result in formal compounding proceedings.

The practical fix: Give your tenant your NRO account details for rent payments. Keep your NRE account only for foreign remittances.

Mistake 2: Not Converting Resident Savings Account to NRO After Becoming NRI

If you move back to India and continue using NRE or NRO accounts without redesignating them to resident accounts, you can face heavy penalties. The reverse is equally true – continuing to use a resident savings account after becoming an NRI is a FEMA violation.

As soon as your NRI status is established – whether by virtue of employment abroad, study abroad or residency in another country – inform your bank and convert your resident account to NRO.

The comparison is straightforward: If the rupee depreciates by 3% against the dollar during your NRE FD tenure, your dollar returns are reduced by 3% – even if the rupee interest rate was higher than the FCNR USD rate. Run the numbers for your specific situation before defaulting to NRE FDs.

Mistake 4: Not claiming DTAA Benefits On NRO Interest

The difference between paying 30% TDS and 15% DTAA rate on NRO interest is significant. On ₹10 lakh of annual NRO interest, that is ₹1.5 lakh in unnecessary tax paid.

Get your TRC from your country of residence’s tax authority. File Form 41 (previously Form 10F) on the Indian income tax portal. Submit both to your bank before the next TDS deduction cycle.

If you deposited foreign salary into your NRO account because it was the only account you had open at the time, that money is now inside the USD 1 million repatriation framework – even though it was foreign income. Restructuring this requires careful planning, Form 145 / Form 146 (previously Form 15CA / Form 15CB) filings.

The right time to plan your account structure is before you need to repatriate – not when you are standing at a bank branch trying to move money urgently.

What Happens to All Three Accounts When You Return to India?

This is one of the most critical and most poorly understood transitions in NRI banking.

- Your NRE account must be converted to a resident account (typically a regular savings account) or to an RFC (Resident Foreign Currency) account

- Your NRO account must be redesignated to a resident account

- Your FCNR deposits can be held until maturity, then converted to RFC accounts

Once you become an RNOR, NRE and FCNR interest remains tax-free for the RNOR period. Once you become a full ROR resident, NRE interest becomes taxable as ordinary income. This is the RNOR window we discussed in our guide on returning NRI tax planning.

The Account Structure Most NRIs Should Have

After reading all of the above, here is the practical recommendation for most NRIs:

If you earn abroad and have Indian income: Keep both NRE and NRO accounts. Route all foreign earnings to NRE, all Indian income to NRO, open FCNR deposits for any substantial foreign currency savings you want to park in India without rupee risk.

If you earn abroad and have no Indian income: NRE account for day-to-day Indian expenses. FCNR deposits for savings. NRO account is technically not needed unless you receive any India-sourced income – but many NRIs open one anyway to handle any incidental Indian receipts.

If you are about to return to India: Review your account balances and consider which funds you want to repatriate before returning (simpler from NRE/FCNR with no limits), plan the account redesignation timing carefully and do not let FCNR deposits mature into the wrong account type.

How FinPracto Helps NRIs Get Their Account Structure Right

At FinPracto, we work with NRIs across the USA, UK, Canada, UAE, Singapore and Australia to ensure their Indian banking structure is FEMA compliant, tax-efficient and set up for smooth repatriation when needed.

Our services include:

- FEMA Compliance Review – Assessing your current account structure and identifying any deposits or transfers that need to be regularised

- TRC and Form 41 Advisory – Helping you obtain your Tax Residency Certificate and file Form 41 (previously Form 10F) to claim DTAA rates on NRO interest

- Form 145 / Form 146 Preparation – Preparation and filing of Form 145 (previously Form 15CA) and Form 146 (previously Form 15CB) for NRO repatriation, with CA certification of tax compliance under IT Rules 2026

- Account Redesignation Guidance – Advising on the sequence and timing of NRE/NRO/FCNR account conversion when returning to India

- FCNR vs NRE Analysis – Running the numbers on currency-adjusted returns for your specific situation and savings amount

- ITR Filing for NRIs – Including NRO interest income, DTAA benefit claims and Schedule FA disclosure of all Indian accounts

- Cross-Border Tax Planning – Ensuring your Indian account income and your foreign return are coordinated and consistent

If you are not sure whether your current account structure is right or if you have been using a resident savings account after becoming an NRI – the right time to fix it is now, before it becomes a formal compliance issue.

Also Read:

- Indian PPF Accounts and US Taxation

- Selling Indian Property as an NRI in 2026

- Transfer Pricing Documentation Under Income Tax Act, 2025

- The Corporate Laws (Amendment) Bill, 2026