If you are an Indian living in the United States – whether on an H-1B, a Green Card, or as a naturalised citizen – there is a very good chance you have money back home.

A savings account in SBI. A fixed deposit your parents manage. A mutual fund you started before moving. An NRO account you opened for rental income, and every year, the US government expects you to report it.

There are two separate reporting requirements. Two different forms. Two different thresholds. Two different deadlines and two very different sets of penalties.

Miss either one – even unknowingly and the consequences can be severe.

This guide breaks down everything you need to know about FBAR (FinCEN Form 114) and FATCA (Form 8938) for 2026, so you always know which one applies to you and when.

Why Do These Two Forms Even Exist?

The US taxes its citizens and residents on their worldwide income regardless of where they live or where their money is held. To enforce this, the government created two parallel disclosure systems:

- FBAR was created under the Bank Secrecy Act of 1970 to track foreign accounts and prevent financial crime.

- FATCA was enacted in 2010 after a series of high-profile offshore tax evasion scandals, to force foreign banks to report US account holders directly to the IRS.

They overlap, but they are not the same, and you may need to file both.

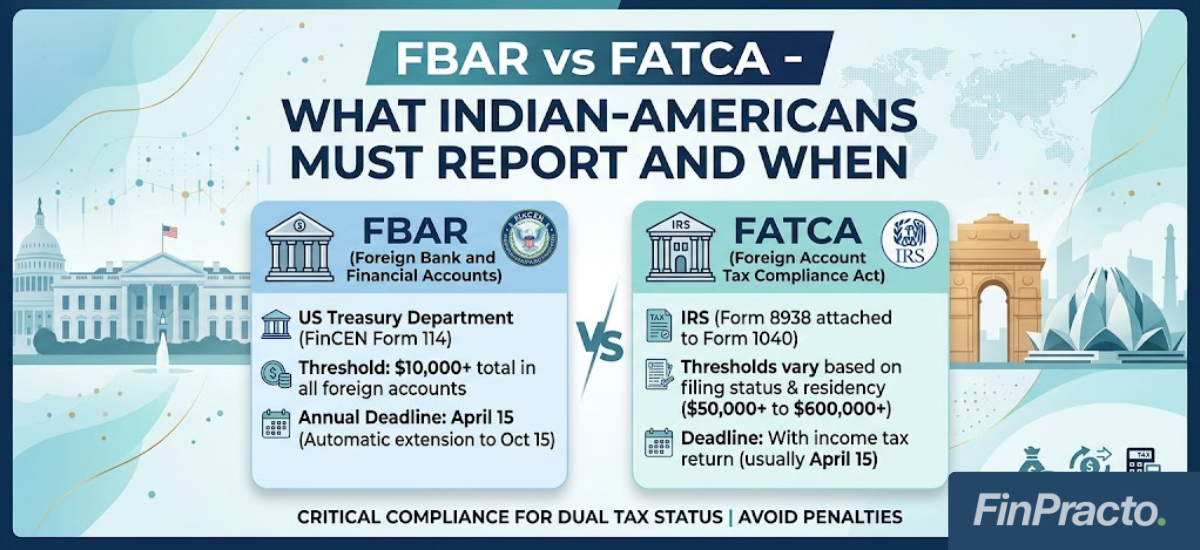

What Is FBAR? (FinCEN Form 114)

FBAR stands for Report of Foreign Bank and Financial Accounts. It is filed using FinCEN Form 114 – not with the IRS but with the Financial Crimes Enforcement Network (FinCEN), a bureau of the US Treasury Department.

Who Must File?

Any US person – citizen, green card holder, or resident alien – who has a financial interest in or signature authority over one or more foreign financial accounts where the aggregate value exceeded $10,000 at any point during the calendar year.

What Counts as a Foreign Financial Account?

- Indian bank accounts (SBI, HDFC, ICICI – any bank outside the US)

- NRO and NRE accounts

- Indian mutual fund accounts held at a financial institution

- Indian brokerage and demat accounts

- Fixed deposits at Indian banks

- Certain life insurance policies with cash surrender value at foreign institutions

Deadlines

- April 15, 2026 – for reporting 2025 calendar year accounts

- Automatic extension to October 15, 2026 – no form or request needed

Important: Filing a US tax extension (Form 4868) does not extend your FBAR deadline. They run on entirely separate timers.

How Is It Filed?

Exclusively online through the BSA E-Filing System at bsaefiling.fincen.treas.gov. Paper filing is not permitted.

What Is FATCA? (Form 8938)

FATCA stands for the Foreign Account Tax Compliance Act. Under FATCA, individuals must file Form 8938 – Statement of Specified Foreign Financial Assets – which is attached directly to your US federal income tax return (Form 1040).

FATCA Thresholds for 2026 (Tax Year 2025)

Thresholds confirmed unchanged for tax year 2025 per IRS guidance. They vary by filing status and where you live.

| Filing Status | Residence | Year-End Value | At Any Point During Year |

| Single / MFS | In the US | More than $50,000 | More than $75,000 |

| Married Filing Jointly | In the US | More than $100,000 | More than $150,000 |

| Single / MFS | Outside the US | More than $200,000 | More than $300,000 |

| Married Filing Jointly | Outside the US | More than $400,000 | More than $600,000 |

What Does FATCA Cover That FBAR Does Not?

FATCA casts a wider net. In addition to foreign bank accounts, Form 8938 requires you to report:

- Foreign stocks and securities held directly (not inside a financial account)

- Interests in foreign partnerships, LLPs and corporations

- Indian PPF, EPF and certain pension accounts

- Foreign life insurance contracts with cash value

- Beneficial interests in foreign trusts and estates

Deadline

Form 8938 is filed with your Form 1040. The deadline is April 15, 2026, with an extension to October 15, 2026 if you file Form 4868.

FBAR vs FATCA – Key Differences at a Glance

| Factor | FBAR (FinCEN Form 114) | FATCA (Form 8938) |

| Filed with | FinCEN (Treasury) | IRS (with Form 1040) |

| Threshold | $10,000 aggregate | $50,000–$600,000 (varies by status & residence) |

| What is reported | Foreign financial accounts | Broader foreign financial assets |

| Deadline | April 15 (auto-extension to Oct 15) | Same as your tax return |

| Direct stock holdings | No | Yes |

| Signature authority triggers filing | Yes | Generally, no |

| Filed separately from tax return | Yes | No – attached to Form 1040 |

The Critical Point Most Indian-Americans Miss

Filing one does not replace the other. This is the single most expensive mistake in this space.

An Indian-American with an NRO account worth $80,000 must file both – FBAR (because it exceeds $10,000) and Form 8938 (because it exceeds the $50,000 US-resident threshold). If you file Form 8938 but skip FBAR, you are still non-compliant and vice versa.

Penalties for Non-Compliance

This is where it gets serious.

FBAR Penalties (2026)

- Non-willful violation: Up to $16,536 per violation (inflation-adjusted)

- Willful violation: The greater of $165,353 or 50% of the account balance per violation, per year

- Criminal penalties: Up to $500,000 in fines and 10 years in prison for wilful non-compliance

FATCA Penalties (Form 8938)

- Failure to file: $10,000 per form

- Continued failure after IRS notice: Additional $10,000 per 30-day period, up to a maximum of $50,000

- Underpayment linked to undisclosed assets: Additional penalty of 40% of the underpayment

Critical point about FATCA: Your foreign bank may already be reporting your account to the IRS. India has signed the FATCA Inter-Governmental Agreement with the US, which means Indian financial institutions are required to report US account holders. Non-disclosure is no longer a safe strategy – it is increasingly a detectable one.

Five Situations Where Indian-Americans Commonly Get This Wrong

Situation 1: “My account is just for family expenses back home”

Purpose does not matter. If the aggregate value crossed $10,000 at any point during the year – even briefly – FBAR is required.

Situation 2: “I only have signature authority, not ownership”

FBAR applies to signature authority too. If you are an authorised signatory on your parents’ Indian bank account or on a company account, you may still have an FBAR obligation – even if you have no financial interest in the funds.

Situation 3: “My NRE account is tax-free in India”

Tax-free status in India has no bearing on US disclosure requirements. NRE accounts are completely exempt from Indian tax but are fully reportable under both FBAR and FATCA.

Situation 4: “I did not earn any income from the account”

Both FBAR and FATCA are disclosure requirements, not just income reporting requirements. Even a dormant account with no transactions must be reported if the threshold is met.

Situation 5: “My Indian mutual funds are not a bank account”

Mutual fund accounts held at Indian financial institutions are reportable under FBAR. Directly held foreign mutual funds and investment interests are additionally reportable under FATCA Form 8938.

What If You Have Never Filed – But Should Have?

Do not panic, but do not delay either. The IRS offers the Streamlined Filing Compliance Procedures for taxpayers whose non-compliance was non-willful (meaning you simply were not aware of the requirement).

Under this program:

- File 3 years of amended tax returns and 6 years of delinquent FBARs

- If you live outside the US: zero offshore penalty

- If you live inside the US: a 5% miscellaneous offshore penalty

The key condition: your failure must have been genuinely non-willful. Taking no action after becoming aware of the requirement changes the classification and the consequences.

India-Specific Assets – Quick Reference

| Asset Type | FBAR Required? | Form 8938 Required? |

| SBI / HDFC / ICICI savings account | Yes (if threshold met) | Yes (if threshold met) |

| NRO account | Yes | Yes |

| NRE account | Yes | Yes |

| Indian fixed deposit | Yes | Yes |

| Indian mutual fund (in demat/financial account) | Yes | Yes |

| Directly held Indian stocks | No | Yes |

| Indian PPF / EPF | Possibly (consult advisor) | Yes |

| Indian life insurance with cash value | Yes | Yes |

| Interest in family-owned Indian company | Possibly | Yes |

How FinPracto Helps Indian-Americans Stay Compliant

At FinPracto, we work with Indian professionals and families across the United States who hold financial ties to India – from tech professionals in Silicon Valley to business owners in New Jersey and Texas.

Our cross-border compliance support includes:

- Assessment of your FBAR and FATCA filing obligations

- Preparation and filing of FinCEN Form 114 (FBAR)

- Preparation of Form 8938 and integration with your US tax return

- Streamlined Filing Compliance Procedures for past non-filers

- Ongoing advisory on NRO, NRE and Indian investment reporting

- India-US DTAA planning to ensure income is not taxed twice

- End-to-end NRI Tax Consultancy – www.finpracto.com/services/tax-planning-advisory-services

We understand both sides of this equation – the Indian asset landscape and the US reporting framework – which means you get advice that is accurate, complete and actionable.

Final Thought

The real risk is not the forms themselves. It is assuming that because your Indian accounts are tax-free in India, they do not need to be reported in the US. That assumption – left unchecked – can turn a simple disclosure into a very expensive problem.