This part covers what happens after that window closes – when you become a full Resident and Ordinarily Resident (ROR) taxpayer. It covers the complete ROR tax treatment, Schedule FA reporting obligations, Black Money Act penalties, withdrawal strategies and answers to the most common questions we receive from returning NRIs managing their HSA.

When does ROR Status actually kick in?

You become ROR only when you satisfy both of the following conditions simultaneously:

- You have been a resident of India in 2 or more of the last 10 financial years, AND

- You have been present in India for 730 days or more during the preceding 7 financial years

For a typical NRI who returns to India in October 2025 after 10 or more years abroad, the timeline looks like this:

| Financial Year | Residential Status | HSA Earnings Taxable in India? | Schedule FA Required? |

| FY 2025-26 | RNOR | No | No |

| FY 2026-27 | RNOR | No | No |

| FY 2027-28 | RNOR | No | No |

| FY 2028-29 | ROR | Yes | Yes |

Most returning NRIs who were abroad for a decade enjoy 3 full financial years of RNOR protection. Use every year of it.

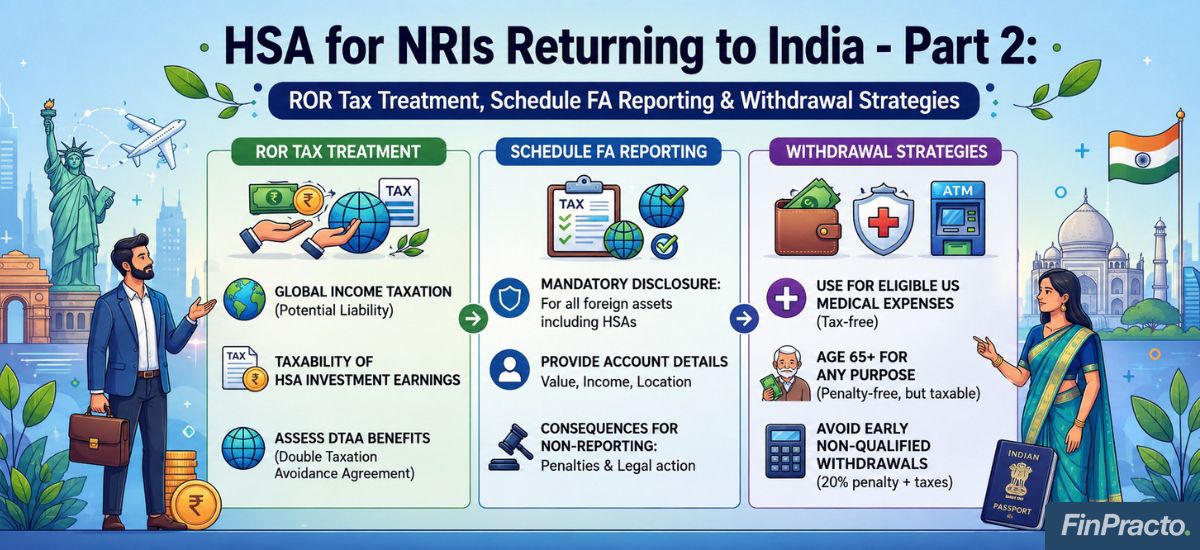

Part A: When you become ROR – The Indian Tax Treatment

What becomes taxable

Once you are ROR, your global income is taxable in India. Under the look-through approach, India taxes only the income earned inside the HSA each year – not the entire balance or withdrawal amount.

| Income Type Inside HSA | Indian Tax Treatment |

| Interest from HSA cash / savings | Taxable as Income from Other Sources at slab rate (up to 30%) |

| Dividends from HSA investments | Taxable as dividend income at slab rate |

| Short-term capital gains | Taxable at slab rate |

| Long-term capital gains | Taxable at 12.5% without indexation under IT Act 2025 |

| Original contributions – the principal | Not taxable – capital, not income |

The annual accrual rule: India taxes HSA income as it is earned – whether or not you withdraw anything. You cannot defer Indian taxation by leaving the money in the account. The moment interest, dividends or capital gains are earned inside the HSA during an ROR year, they are taxable in India for that year.

Are Withdrawals separately taxed in India?

If you have correctly reported and paid Indian tax on the underlying HSA income annually as it accrued, the withdrawal itself does not create a separate Indian tax event. India taxes income, not capital and a withdrawal of previously taxed earnings is not a second income event.

The practical approach: Report and pay Indian tax on HSA earnings every year as an ROR taxpayer. Withdrawals from earnings that have already been taxed should not trigger additional Indian tax.

DTAA – Why it does not help the HSA

The India-US DTAA provides no specific exemption for HSA income. The treaty was signed decades before HSAs were created in 2003 and does not mention them. Since HSA earnings are tax-free in the US, there is no US tax paid to use as a foreign tax credit in India. The full Indian tax rate applies with no offset.

The Critical Contrast – HSA vs 401(k) and IRA

| Account | Section 89A Deferral? | Indian Tax on Annual Accrual | Best Approach as ROR |

| 401(k) / Traditional IRA | Yes | Deferred until withdrawal | Hold – Section 89A protects annual growth |

| Roth IRA | Yes | Deferred until withdrawal | Hold – Section 89A protects annual growth |

| HSA | No | Taxable every year | Draw down first – no deferral benefit |

Since the HSA receives no Section 89A relief while retirement accounts do, the HSA should be drawn down before 401(k) and IRA accounts in your ROR years. This reduces the annual Indian tax drag from HSA earnings while allowing your retirement accounts to continue compounding under Section 89A protection.

Part B: Schedule FA – Mandatory Reporting once you are ROR

Who must file and Who is Exempt

Schedule FA is mandatory only for ROR taxpayers. NRIs and RNORs are fully exempt. The moment you become ROR, Schedule FA becomes a mandatory annual filing – every year for as long as you remain ROR and hold any foreign asset.

How to classify your HSA in Schedule FA

Report your HSA under Table A2 – Foreign Custodial Accounts in Schedule FA. This is the standard classification for US financial accounts holding investments managed by a custodian – which is how most HSAs that invest in mutual funds or ETFs are structured.

The Calendar Year Rule – A Detail many miss

Schedule FA follows the calendar year (January 1 to December 31) – not India’s financial year (April 1 to March 31). For AY 2026-27 (FY 2025-26), you must report all foreign assets held at any point between January 1, 2025 and December 31, 2025.

This means: If you became ROR in April 2028 but held your HSA throughout calendar year 2028, you must report it in Schedule FA for that year – even though your ROR status only began on April 1, 2028.

What to include in Schedule FA for Your HSA

- Name of financial institution and country (USA)

- HSA account number

- Opening balance (in USD and INR at RBI reference rate)

- Closing balance at December 31 (in USD and INR)

- Interest, dividends and capital gains earned during the calendar year

- Amount withdrawn during the year

- INR equivalent of each figure using RBI reference exchange rates for the relevant dates

Maintain annual HSA statements, brokerage confirmations and exchange rate records for every year you are ROR.

The Black Money Act Penalty

Failing to disclose foreign assets in Schedule FA as an ROR taxpayer attracts a penalty of ₹10 lakh per year of default under the Black Money Act, 2015. This applies even if the asset generated no income during the year. In serious cases of wilful non-disclosure, prosecution and imprisonment of up to 7 years is also possible.

This penalty is not proportionate to the asset’s value. Whether your HSA holds $5,000 or $500,000, the penalty for non-disclosure as an ROR is ₹10 lakh per year.

If you have missed Schedule FA in earlier ROR years: The FAST-DS 2026 scheme – once its commencement date is officially notified – provides a voluntary disclosure window with significantly reduced penalties and immunity from prosecution. Speak to a qualified advisor immediately to assess your exposure.

Part C: Withdrawal Strategies

Strategy 1: Exhaust Qualified Medical Expenses First

The most tax-efficient withdrawal from an HSA – in the US and in India – is always for qualified medical expenses. Under IRS rules, you can reimburse yourself for any qualified medical expense incurred since you opened your HSA, regardless of when you make the withdrawal. There is no statute of limitations on HSA medical reimbursements.

This means: every medical bill from your years in the US that you paid out-of-pocket and never claimed from your HSA is a tax-free withdrawal waiting to happen. Gather every receipt, going back to the date your HSA was first opened.

For Indian medical expenses during RNOR: the IRS allows HSA withdrawals for qualified medical expenses regardless of where the care was received. Indian hospital bills, doctor fees and prescriptions all qualify – but documentation must be meticulous: Itemised bills in INR, currency conversion to USD at date of service and confirmation the expense was not reimbursed by insurance.

Strategy 2: The Age 65 Rule

Once you turn 65, the 20% early withdrawal penalty on non-medical HSA withdrawals disappears entirely. From age 65, you can withdraw any amount for any reason – paying only ordinary US income tax on the withdxdawal, with no penalty.

For returning NRIs who are 60 or older, this changes the calculation significantly. Waiting until 65 means the only US cost is income tax – which, combined with any available Indian foreign tax credit, may result in a manageable total tax position.

Strategy 3: Draw Down HSA Before Your Retirement Accounts as ROR

As covered above – your 401(k) and IRA benefit from Section 89A deferral while your HSA does not. As an ROR taxpayer, every year your HSA earns income creates an Indian tax liability. Every year your 401(k) earns income while Section 89A is elected, it does not.

The logical sequencing: draw down the HSA first, eliminating its annual Indian tax drag, while allowing the retirement accounts to continue growing under Section 89A protection.

Strategy 4: Document Everything

Regardless of which strategy applies to your situation, documentation is non-negotiable:

- Annual HSA statements showing opening balance, closing balance, contributions, withdrawals and earnings breakdown

- Itemised medical expense receipts for every qualified withdrawal — dated, from a licensed provider, with clear description of the service

- For Indian medical expenses: original bills in INR, exchange rate conversion at date of service, and proof of payment

- Annual RBI reference exchange rate records for INR-USD conversion in Schedule FA

How FinPracto helps

At FinPracto, we work with Indians across the US – H-1B professionals, Green Card holders and US citizens returning to India – who need coordinated US and Indian tax advice on their HSA, 401(k), IRA and brokerage accounts through the transition. Our cross-border services for HSA planning include:

- RNOR window calculation – Precise determination from your actual travel records

- Pre-return HSA strategy – Withdrawal timing, medical reimbursement planning, final-year contribution maximisation

- Indian ITR filing – Annual characterisation of HSA income under the look-through approach

- Schedule FA preparation – Complete foreign asset disclosure with correct valuation and income breakdown

- Black Money Act advisory – Prior-year non-disclosure exposure assessment and FAST-DS 2026 guidance

- Section 89A coordination – Integrating HSA planning with 401(k) and IRA strategy

- India-US return coordination – Consistent ITR and Form 1040 positions with no unrelieved double taxation

Final Thought

Your HSA is a valuable asset built over years of disciplined saving. It was designed for the US tax system – but with the right planning, it can be managed through a return to India without unnecessary tax cost.

The RNOR window gives you years of planning time. The look-through approach means India taxes income, not capital. The age-65 rule eliminates the early withdrawal penalty at the right moment for many returning NRIs and the documentation habits – annual statements, expense receipts, exchange rate records – are entirely manageable once you know what is required.

Start planning before you return. Not after your first ROR tax year.