Cross-border consultancy arrangements – especially involving UAE-based professionals and foreign group entities – often face scrutiny from Indian tax authorities. A recent ruling by the Income Tax Appellate Tribunal (ITAT) has once again clarified when such income cannot be taxed in India.

Case: Vijay Mariappan Austin Prakash v. ACIT (International Taxation)

Citation: ITA No. 89/VIZ/2025 (ITAT Visakhapatnam)

Order Date: 05 December 2025

The assessee, a UAE resident consultant, provided consultancy services in relation to Indian projects. The key issue was whether such receipts – either directly or through associated foreign entities – could be taxed in India.

What Triggered the Dispute?

The tax authorities argued that:

- Consultancy services were linked to India, hence taxable under Section 9 of the Income-tax Act.

- Income could be classified as Fees for Technical Services (FTS).

- The assessee had sufficient presence in India to trigger taxability under the India–UAE DTAA.

What the ITAT Held?

The Tribunal rejected the tax department’s position and ruled in favour of the assessee, laying down clear principles:

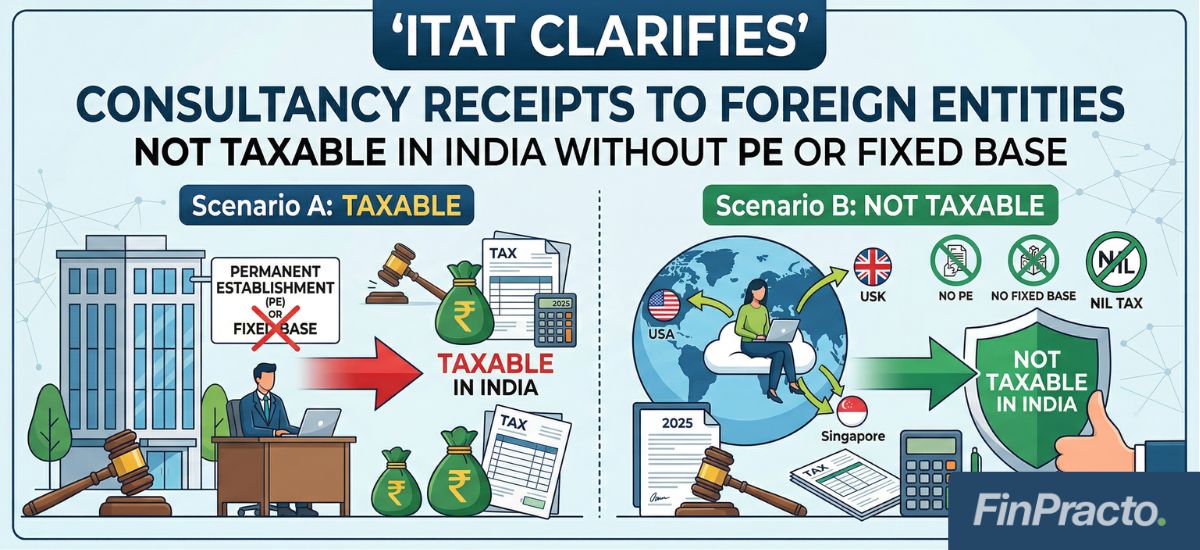

1. No Fixed Base = No Tax under DTAA

Under Article 14 (Independent Personal Services) of the India–UAE DTAA:

- Taxability arises only if the individual has a fixed base in India or

- Stays in India for 183 days or more

In this case:

- No fixed base was established

- Stay in India was below the threshold

Result: Income not taxable in India

2. Mere Link to Indian Projects is Not Enough

The Tribunal emphasized:

- Just because services relate to Indian projects does not mean they are rendered in India

- Taxability depends on where and how services are performed, not merely the end-use

Result: No business connection or taxable nexus established

3. FTS Classification Cannot Be Assumed

The tax authorities attempted to treat the income as Fees for Technical Services (FTS)

However:

- There was no evidence of technical knowledge being “made available”

- Consultancy or advisory services do not automatically qualify as FTS

Result: Not taxable as FTS

4. DTAA Overrides Domestic Law

The Tribunal reaffirmed that under Section 90(2):

- The assessee can choose provisions of the DTAA if they are more beneficial

Result: Treaty protection prevailed over domestic tax provisions

Key Takeaways for Businesses & Consultants

- UAE-based consultants are not automatically taxable in India for India-related work

- No PE / Fixed Base = No tax exposure under the India–UAE DTAA

- Short-term presence in India does not trigger taxation

- Consultancy ≠ FTS, unless specific technical conditions are met

- Proper structuring and documentation of services is critical

Why This Matters?

This ruling is particularly important for:

- UAE-based professionals and consultants

- Non-resident Indians (NRIs) providing advisory services

- Businesses routing consultancy through foreign group companies

- Startups and global firms working on India-linked projects

It reinforces a key principle: Indian taxability depends on substance, not assumptions.

How FinPracto Helps?

At FinPracto, we assist clients in navigating complex cross-border tax situations by:

- Structuring tax-efficient consultancy arrangements

- Evaluating PE / Fixed Base exposure in India

- Advising on FTS classification and DTAA positions

- Supporting in litigation and reassessment matters

- Ensuring robust documentation and compliance

The ITAT’s ruling brings welcome clarity – consultancy income earned by UAE residents cannot be taxed in India unless clear treaty conditions are met.

For businesses and professionals operating across borders, this is a strong reminder that Correct structuring + DTAA Understanding = Tax certainty.