The Reality: Market Entry Starts with People But Tax Starts Immediately

Many foreign companies enter India by deploying employees before setting up an entity. It’s fast, flexible and commercially sensible. However, from a tax standpoint, this is not a neutral step.

The moment employees start operating in India, tax exposure may already begin.

The mistake most companies make is assuming that structuring (secondment or EOR) determines tax outcomes. It doesn’t. What matters is control, function and economic reality.

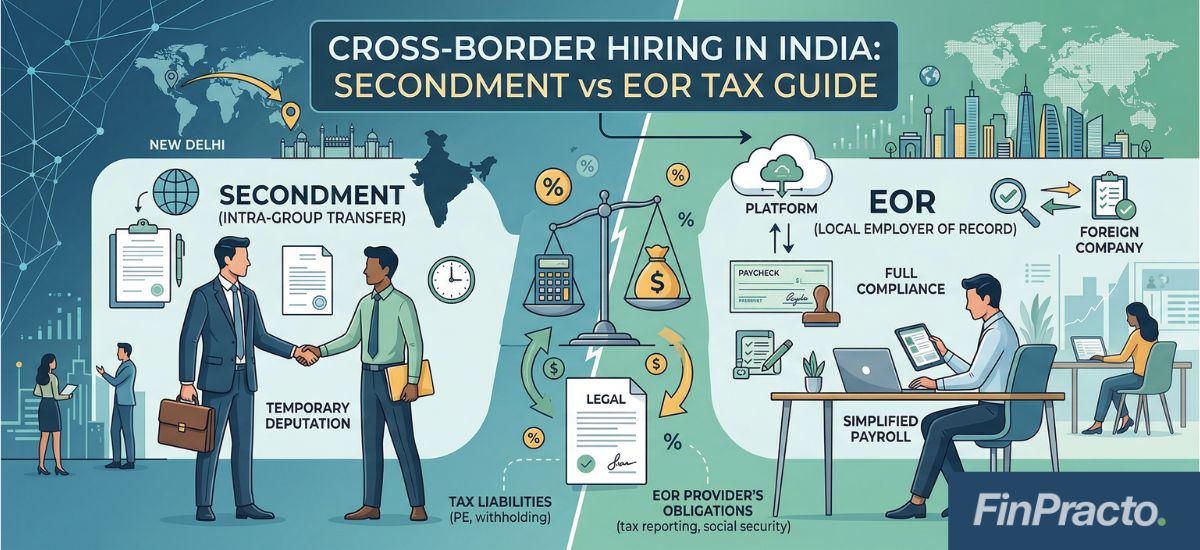

Secondment: Where Most Structures Fail in Practice?

Secondment is often used with the assumption that keeping employees on foreign payroll avoids Indian tax complexity. In reality, Indian tax authorities focus on three things:

- Who controls and directs the employee’s work

- Who benefits from the work performed

- Who ultimately bears the cost

If these point to the Indian side, the arrangement is treated as local employment, regardless of how contracts are drafted.

What this Means in Practice:

- Salary becomes taxable in India

- Indian withholding (TDS) obligations apply

- “Reimbursement” structures lose their intended tax neutrality

If not structured carefully, what was meant to be a temporary deployment becomes a fully taxable presence.

EOR Model: Operationally Easy, Structurally Risky

The Employer of Record (EOR) model is increasingly popular because it allows companies to “hire in India without setting up in India.” However, from a tax perspective, this model is often misunderstood. The critical question is whether the EOR:

- is a true employer, or

- Merely a compliance and payroll layer

If the foreign company continues to assign work, evaluate performance or control deliverables then the EOR structure may not hold up under scrutiny. In such cases, tax authorities may effectively ignore the EOR layer.

Permanent Establishment (PE): The Risk that Changes Everything

This is the point most businesses underestimate. A Permanent Establishment (PE) can be triggered even without:

- Incorporation

- Registration

- or a Physical office

All it takes is people performing core business functions in India. Typical triggers include:

- Employees contributing to revenue generation

- Involvement in contract negotiation or execution

- Acting as a key interface for Indian operations

Once a PE is established: The foreign company becomes taxable in India on attributable profits. What started as a low-risk entry strategy can quickly turn into a full tax exposure scenario.

What the Latest Tax Position Reinforces?

Tax follows substance – not structure.

- Labels like “secondment” or “EOR” do not determine outcomes

- Documentation without operational alignment does not hold

- Employee presence is independently capable of creating tax liability

What Smart Companies Do Differently?

Companies that get this right focus less on form and more on defensibility.

In practice, this means:

- Clearly defining who controls the employee in reality

- Ensuring contracts reflect actual working relationships

- Evaluating PE exposure before deployment – not after

Most tax disputes in this space arise because structuring is done for convenience, not for sustainability.

Why FinPracto Becomes Critical at This Stage?

This is not an area where generic compliance works. Early structuring decisions directly impact long-term tax exposure in India. At FinPracto, we work with foreign companies at the entry stage – helping them move from initial employee deployment to a well-structured and compliant India presence.

We assist in:

- End-to-end India entry, including subsidiary incorporation and group structuring

- Advising on the right approach between secondment, EOR or direct entity setup

- Designing structures that withstand tax and regulatory scrutiny

- Assessing Permanent Establishment risk upfront

- Ensuring withholding, payroll and ongoing compliance are aligned from day one

Cross-border employee deployment is often the first tax trigger point in India. Getting it right early enables smooth expansion; getting it wrong can lead to exposure that surfaces later in audits and litigation.